The Emergency Credit Line Guarantee Scheme (ECLGS) stands out as one of India’s most decisive financial interventions in recent years. What began as a crisis-response mechanism during the COVID-19 pandemic has now evolved into a long-term economic support system. In 2026, the scheme continues to play a critical role as global uncertainties, supply chain disruptions, and geopolitical tensions put pressure on businesses.

Here’s what matters. ECLGS is not just a loan scheme. It is a confidence mechanism. When businesses struggle, banks hesitate to lend due to risk. This scheme removes that hesitation by offering a government-backed guarantee. That single feature unlocks credit when it is needed the most.

With the launch of ECLGS 5.0 in 2026, the government has reinforced its commitment to protecting MSMEs, stabilizing key sectors like aviation, and ensuring uninterrupted economic activity. This article breaks down every aspect of the scheme including its structure, evolution, RBI guidelines, ministry involvement, UPSC relevance, and latest updates.

What is Emergency Credit Line Guarantee Scheme (ECLGS)?

The Emergency Credit Line Guarantee Scheme (ECLGS) is a government-backed initiative that provides collateral-free loans to businesses through banks and financial institutions.

Banks provide loans to businesses facing financial stress. Normally, banks would worry about repayment risks. Under ECLGS, the government guarantees a major portion, often up to 100 percent, of these loans. This reduces risk for lenders and ensures quick credit flow.

The scheme is implemented through the National Credit Guarantee Trustee Company (NCGTC), which provides the guarantee coverage.

Core Objective

The primary aim of ECLGS is straightforward:

- Ensure liquidity in the market

- Support MSMEs and key industries

- Protect jobs and economic stability

This makes it one of the most important policy tools for economic recovery and crisis management.

Emergency Credit Line Guarantee Scheme Launch Date

The scheme was officially launched in May 2020 as part of the Atmanirbhar Bharat economic relief package.

Initially, it was designed to help businesses survive the COVID-19 lockdown and economic slowdown. However, its success led to multiple extensions and upgrades.

Evolution of ECLGS

The scheme has gone through several phases:

- ECLGS 1.0 (2020) – Focused on MSMEs with basic credit support

- ECLGS 2.0 – Extended to larger businesses and stressed sectors

- ECLGS 3.0 – Targeted hospitality, tourism, and healthcare

- ECLGS 4.0 – Expanded healthcare support during pandemic waves

- ECLGS 5.0 (2026) – Designed to tackle global economic disruptions

This phased expansion shows that ECLGS is not static. It adapts based on economic needs.

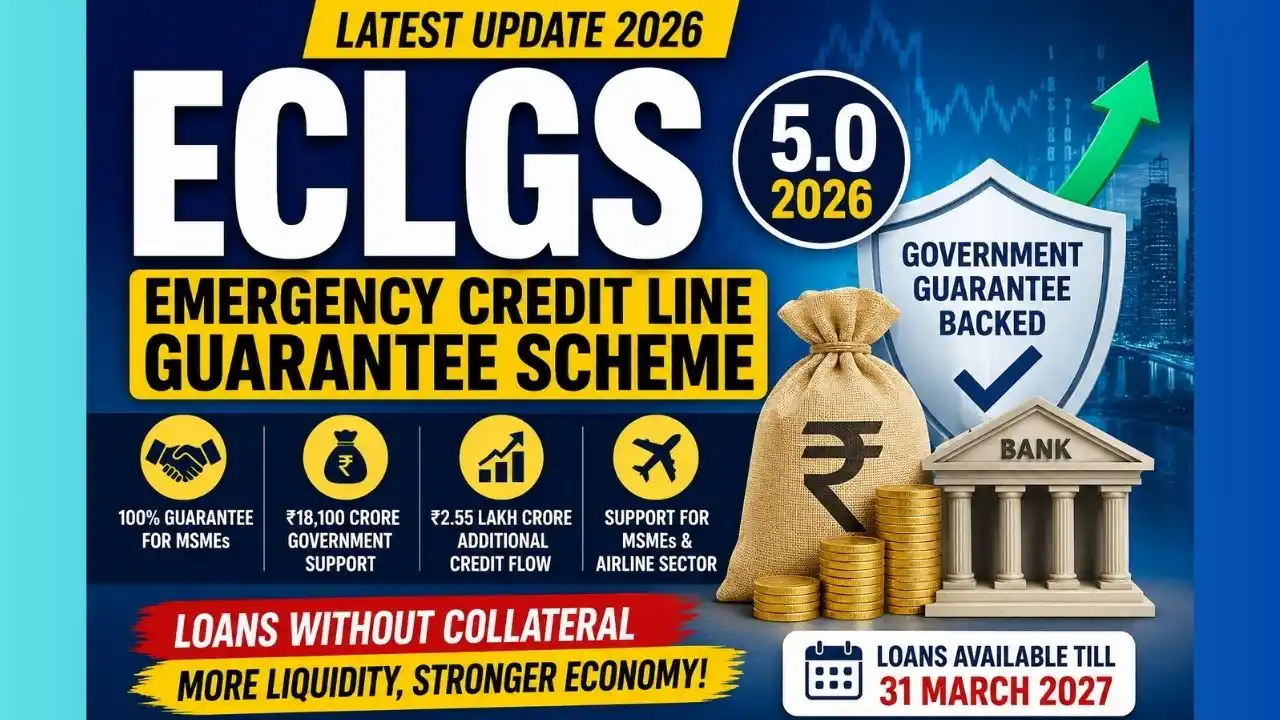

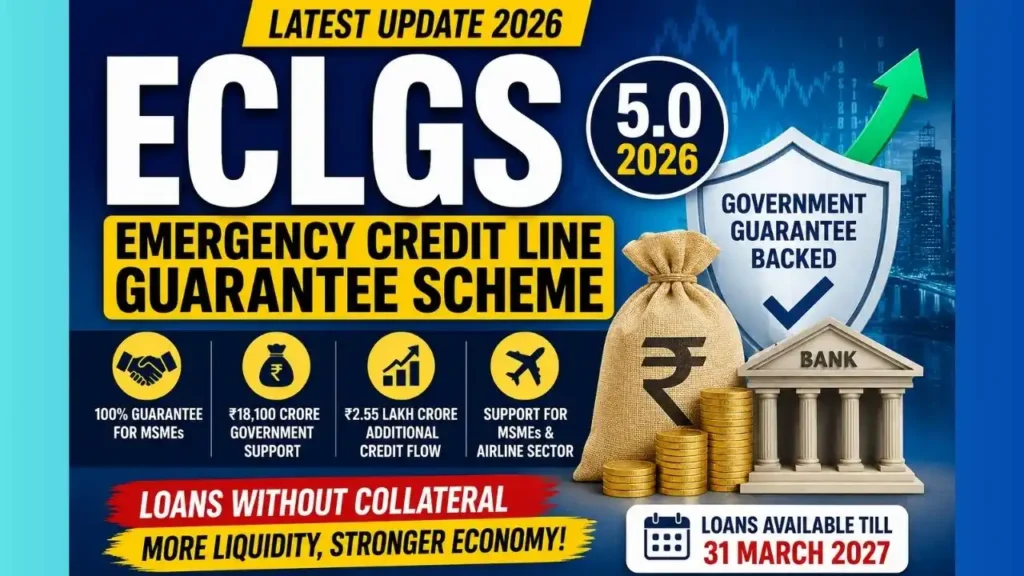

Emergency Credit Line Guarantee Scheme 2026 (Latest Update)

In 2026, the Government of India introduced ECLGS 5.0 to address challenges arising from global geopolitical tensions, including disruptions in trade and rising operational costs.

Key Highlights of ECLGS 5.0

- ₹18,100 crore government guarantee backing

- ₹2.55 lakh crore expected additional credit flow

- Special focus on MSMEs and airline sector

- Loan availability extended till March 31, 2027

- 100% guarantee for MSMEs

- 90% guarantee for other sectors

Why ECLGS 5.0 Matters

Here’s the real impact.

Global conflicts have increased fuel costs, disrupted logistics, and affected demand. Businesses, especially MSMEs, face cash flow problems. Without intervention, this can lead to shutdowns and job losses.

ECLGS 5.0 ensures:

- Businesses continue operations

- Employment remains stable

- Financial institutions keep lending

This version confirms that the scheme has evolved into a long-term economic shock absorber.

Emergency Credit Line Guarantee Scheme Under Which Ministry?

The scheme operates under the Ministry of Finance, Government of India.

Institutional Framework

- Department of Financial Services (DFS) – Oversees implementation

- NCGTC – Provides guarantee coverage

- Banks and NBFCs – Disburse loans

This structure ensures coordination between policy-making, guarantee management, and credit delivery.

Guaranteed Emergency Credit Line (GECL) Explained

The Guaranteed Emergency Credit Line (GECL) is the actual loan provided under ECLGS.

Think of it like this:

- ECLGS is the scheme

- GECL is the loan product

Key Features of GECL

- Collateral-free loans

- Additional credit based on existing loans

- Government-backed guarantee

- Faster approval with minimal documentation

Why GECL is Important

Banks usually avoid lending during uncertain times. GECL reduces their risk. Since repayment is guaranteed by the government, lenders are more willing to extend credit.

This directly improves liquidity in the economy.

Emergency Credit Line Guarantee Scheme RBI Circular PDF

The Reserve Bank of India (RBI) plays a key role in aligning the scheme with banking regulations.

RBI circulars related to ECLGS provide operational guidelines for banks.

Key Areas Covered in RBI Circulars

- Loan eligibility criteria

- Restructuring guidelines

- Repayment terms and moratorium

- Asset classification norms

- Reporting requirements

Why RBI Circular is Important

For banks, the RBI circular acts as a rulebook. It ensures uniform implementation across institutions.

For students and professionals, especially those preparing for exams, the RBI circular provides practical insights into how policy translates into action.

Eligibility Criteria Under ECLGS

Eligibility has changed across different versions, but some common criteria remain consistent.

For Businesses

- Must be an existing borrower

- Loan account should be standard (not NPA)

- Must meet defined credit limits

For MSMEs

- Credit exposure within specified limits

- Account should not have high overdue days

For Larger Businesses

- Higher credit thresholds introduced in later phases

- Sector-specific eligibility criteria

One limitation to note is that new businesses without prior loans are generally not covered.

Loan Features and Benefits

ECLGS offers several borrower-friendly features.

1. Collateral-Free Loans

Businesses are not required to provide additional security, which improves accessibility.

2. Government Guarantee

Up to 100% guarantee for MSMEs reduces lender risk significantly.

3. Moratorium Period

Borrowers usually get a 1 to 2 year moratorium on principal repayment.

4. Flexible Tenure

Loan tenure typically ranges from 4 to 7 years.

5. No Guarantee Fee

Banks do not pay guarantee fees, making the scheme cost-effective.

These features make ECLGS highly attractive compared to traditional loans.

Objectives of Emergency Credit Line Guarantee Scheme

The scheme is built around clear economic goals.

1. Provide Immediate Liquidity

Businesses facing cash shortages can access funds quickly.

2. Support MSME Sector

MSMEs contribute significantly to GDP and employment.

3. Protect Employment

By supporting businesses, the scheme indirectly safeguards jobs.

4. Stabilize Financial System

Prevents widespread defaults and reduces banking stress.

Emergency Credit Line Guarantee Scheme UPSC Notes

ECLGS is highly relevant for UPSC aspirants, especially in Economics and Current Affairs.

Key Facts

- Launch Year: 2020

- Ministry: Finance

- Implementing Agency: NCGTC

- Target: MSMEs and stressed sectors

- Type: Credit guarantee scheme

Prelims Focus

- Full form of ECLGS

- Launch timeline

- Guarantee coverage

Mains Focus

- Role in economic recovery

- Impact on MSMEs

- Fiscal implications

Sample Question

Discuss the role of ECLGS in stabilizing India’s economy during crises.

Impact of ECLGS on Indian Economy

The scheme has delivered measurable results.

1. Boost to MSMEs

Millions of small businesses received financial support, helping them survive disruptions.

2. Increased Credit Flow

Banks were able to lend more due to reduced risk.

3. Job Protection

The scheme helped prevent layoffs across multiple sectors.

4. Sectoral Stability

Industries like tourism, healthcare, and aviation benefited significantly.

Overall, ECLGS played a crucial role in maintaining economic continuity.

Challenges and Criticism

Despite its success, the scheme has faced criticism.

1. Limited Reach Initially

Some small and informal businesses struggled to access the scheme.

2. Dependency on Existing Loans

New businesses without credit history were excluded.

3. Risk of Future NPAs

Since the government guarantees loans, it may face financial burden if defaults rise.

These concerns highlight areas for improvement in future versions.

Future of Emergency Credit Line Guarantee Scheme

Looking ahead, the scheme is likely to evolve further.

Possible Developments

- Expansion to startups and new businesses

- Integration with digital lending platforms

- Inclusion of green and sustainable financing

- Sector-specific targeted support

The 2026 update makes one thing clear. ECLGS is no longer temporary. It is becoming a permanent tool for economic resilience.

Frequently Asked Questions (FAQs) Emergency Credit Line Guarantee Scheme

– What is the Emergency Credit Line Guarantee Scheme (ECLGS)?

The Emergency Credit Line Guarantee Scheme (ECLGS) is a government-backed loan scheme that provides collateral-free credit to businesses, especially MSMEs. Under this scheme, the government guarantees repayment to banks, which encourages them to lend money during financial stress.

– Who is eligible for ECLGS in 2026?

Eligibility mainly includes existing borrowers such as MSMEs and businesses with active loan accounts that are not classified as NPAs. In ECLGS 5.0, the scheme also targets sectors like aviation and businesses affected by global economic disruptions.

– What is the difference between ECLGS and GECL?

ECLGS is the overall scheme, while GECL (Guaranteed Emergency Credit Line) is the actual loan provided under the scheme. In simple terms, ECLGS is the policy and GECL is the financial product businesses receive.

– Is collateral required under ECLGS loans?

No, loans provided under ECLGS are completely collateral-free. This is one of the biggest advantages of the scheme, making it easier for small businesses to access funds without pledging assets.

– What is the latest update in ECLGS 5.0 (2026)?

The latest version, ECLGS 5.0, includes a government guarantee of ₹18,100 crore and aims to generate ₹2.55 lakh crore in additional credit. It focuses on MSMEs and the airline sector, with loan availability extended till March 31, 2027.

Conclusion

The Emergency Credit Line Guarantee Scheme (ECLGS) has transformed from a pandemic relief measure into a powerful financial safety net for India’s economy. Its core strength lies in a simple but effective idea: reduce risk for lenders and increase access to credit for businesses.

With ECLGS 5.0, the government has shown that it is ready to respond quickly to global challenges and protect domestic industries. The scheme continues to support MSMEs, stabilize key sectors, and ensure economic continuity.

Bottom line. ECLGS is not just about loans. It is about trust, stability, and economic confidence. And as long as uncertainties exist, this scheme will remain a critical pillar of India’s financial strategy.

Also read:-

Manoj Talukdar is a content writer and researcher at Assam Guwahati, focusing on government schemes, Assam-related updates, education, finance, and public welfare programs. Through assamguwahati.com, he publishes informative articles, guides, and scheme updates to help readers understand benefits, eligibility requirements, and application procedures.